Decoding the Draft Income-Tax Rules, 2026: Major Changes to Payroll, Perquisites, and Compliance

The Central Board of Direct Taxes (CBDT) has decided to replace the six-decade-old Income-tax Rules of 1962 for which they have released the Draft Income-tax Rules, 2026. Slated to come into effect on April 1, 2026, and, alongside the new Income Tax Act, 2025, this overhaul is a monumental step toward digital transformation and administrative simplicity. The CBDT has drastically reduced the total number of rules from 511 to 333 and the number of tax forms from 399 to 190.

For HR professionals, finance teams, and employees, these draft rules introduce massive shifts in how employee benefits are valued, how TDS is reported, and how businesses manage their monthly payroll cycles.

In this article we deep-dive of the core objectives behind this change, the direct impact on payroll, and how your business can proactively prepare.

The Core Objective: Ease of Doing Business & Digital First

Due to friction faced by businesses and its employees, to enhance the “ease of living and ease of doing business” across India, the overarching goal of the Draft Income-tax Rules, 2026 sets the tone. The government is moving away from complex, manual paperwork and actively shifting toward a highly automated, data-driven tax ecosystem.

Key Benefits:

- Reduction of Interpretational Disputes: By simplifying the legal language and clearly setting reporting thresholds, the government aims to drastically reduce tax litigation between businesses and tax authorities.

- “Smart” Automated Forms: The new, redesigned tax forms emphasize standardization of common information to eliminate repetitive data entry and feature advanced pre-fill capabilities that cross-reference data automatically.

- Faster, Faceless Assessments: Clean, structured digital data allows the Income Tax Department to process returns centrally and resolve assessments faster, minimizing the need for businesses to interface personally with tax officials.

For businesses, following these rules is not just about avoiding penalties; it is about embracing operational efficiency. Companies that align their internal software with these “Smart Forms” will see a massive reduction in the manual hours spent on year-end tax compliance.

House Rent Allowance (HRA) – Expanded Metro Coverage & Enhanced Compliance

Expansion of Metro Cities (50% limit)

Under the earlier rules, HRA exemption up to 50% of Basic+DA was available only for employees residing in Mumbai, Delhi, Kolkata, and Chennai. The Draft Rules expand the metro city list to include:

- Hyderabad

- Pune

- Ahmedabad

- Bengaluru

Employees residing in the above cities will now be eligible for HRA exemption up to 50% of salary, subject to other conditions.

Strengthened HRA Compliance Requirements

The Draft Rules propose stricter compliance for HRA claims, including:

- Mandatory disclosure of the relationship between the employee and landlord.

- Collection and retention of rent agreement documentation by the employer.

Employers must urgently revisit their HRA documentation and verification processes to accommodate these new disclosure requirements.

Leave Travel Allowance (LTA) – Air Travel Rule Rationalised

The rules surrounding Leave Travel Concession (LTC) have been updated to reflect modern corporate travel standards:

- The restriction of limiting tax exemption strictly to economy class airfare is removed.

- LTC exemption will now apply to the class airfare to which the employee is entitled, in addition to their respective company policy.

- This also includes recognised public transport, as applicable.

Allowances & Perquisite Valuation – Revised Limits

The Draft Income-tax Rules, 2026 propose a substantial revision in exemption limits and perquisite valuation amounts to align them with current market costs and inflation.

Comparison of Existing Rules vs Draft Rules

Item | Earlier Rules | Draft Rules – 2026 |

Children Education Allowance (Limit to 2 children) | ₹100 per month per child | ₹3,000 per month per child |

Hostel Allowance | ₹300 per month per child | ₹9,000 per month per child |

Meals (Applicable to Old & New Tax Regime) | ₹50 per meal (Monthly limit ₹2,200) | ₹200 per meal (Monthly limit ₹8,800) |

Gifts (non-cash) | ₹5,000 per year | ₹15,000 per year |

Motor Car (≤ 1.6 litres) | ₹1,800 per month | ₹5,000 per month |

Motor Car (> 1.6 litres) | ₹2,400 per month | ₹7,000 per month |

Driver Salary | ₹900 per month | ₹3,000 per month |

Old Tax Regime vs New Tax Regime – Position under Draft Rules, 2026

The suitability of the Old or New Tax Regime will continue to depend on individual income levels and available exemptions. However, the Draft Rules heavily alter the strategic landscape:

- With enhanced exemption limits for allowances (like Education, Hostel, and expanded 50% HRA) and perquisites, the Old Tax Regime may become highly beneficial for high-salaried employees when combined with 80C and other deductions.

- Employees who earlier found the Old Regime less beneficial may see improved tax outcomes due to these massively revised limits.

Important Note: These specific tax rule allowance changes (like HRA and Education Allowance) will be applicable primarily for employees opting for the Old Tax Regime.

New Structured TDS Compliance (Rule 204)

The Draft Income-tax Rules, 2026 introduce a highly structured mechanism for how employees declare income and how employers deduct TDS under Section 392(1).

- For Employees (Form No. 122): Instead of ad-hoc declarations, employees will use a standardized Form No. 122 to submit details of income from previous employers, house property losses, and prior TDS/TCS deductions to their current employer.

- For Employers (Form No. 123 & 130): Employers are now explicitly required to furnish a detailed statement of perquisites and profits in lieu of salary. This is reported via Form No. 130 (for salaries up to ₹1,50,000) or Form No. 123 (for salaries above ₹1,50,000).

Note: For the purposes of this rule, “Salary” carries the same meaning as defined in Rule 15 of the new Draft Rules (which includes basic pay, allowances, and variable pay, but excludes the value of the perquisites themselves).

Changes in Proposed Forms – Old vs New Reference Numbers

One of the most impactful changes under the Draft Income-tax Rules, 2026 is the complete renumbering and restructuring of statutory forms. Every form that HR teams, Finance departments, employees, and payroll softwares currently process on a daily basis is being replaced. Understanding this mapping is critical to avoiding the use of outdated forms after April 1, 2026.

1. Change in PAN Application Form Numbers

The forms used to apply for a Permanent Account Number (PAN) are being renumbered:

- Form No. 49A (PAN application for Indian citizens/entities) is proposed to be replaced by Form No. 93.

- Form No. 49AA (PAN application for foreign citizens/entities) is proposed to be replaced by Form No. 95.

2. Change in Employee Declaration Form

Form No. 124 (showing particulars of claims by an employee) is proposed to replace the widely used Form No. 12BB. This is the form that every salaried employee submits to their employer at the beginning of the financial year to declare their expected tax-saving investments and exemptions.

Under the new Form No. 124, employees must now mandatorily disclose:

- HRA Exemption Claims: Including the relationship with the landlord (if any) and supporting rent agreement documentation.

- Leave Travel Allowance (LTA) Details: Including the class of travel and mode of transport.

- Housing Loan Details: Both interest and principal repayment amounts.

- Other Deductions and Exemption Claims: Any other declarations under applicable sections.

This is a significant upgrade from the older Form 12BB, as it now explicitly demands landlord relationship disclosures and more granular travel-related proofs, tightening the entire investment declaration process.

3. Change in TDS Certificate for Salaried Employees

Form No. 130, the certificate for tax deducted at source on salary paid to an employee, pension, or interest paid to a specified senior citizen, is proposed to replace the universally recognised Form No. 16.

Key structural differences:

- The earlier Form No. 16 had two parts (Part A and Part B).

- The new Form No. 130 has three parts, with an additional annexure introduced specifically for senior citizens in applicable cases.

This additional part consolidates pension income and senior citizen-specific tax information that was previously handled separately.

4. Change in TDS Certificate for Non-Salaried Individuals

Form No. 131 is the revised TDS certificate issued to non-salaried persons, replacing the earlier Form No. 16A. This form is relevant for vendors, contractors, and service providers from whom TDS is deducted on non-salary payments such as professional fees, rent, and commissions.

5. Change in Quarterly TDS Statement for Salary

The quarterly TDS statement for salary payments, currently submitted as Form No. 24Q, is proposed to be renumbered as Form No. 138. This statement must be submitted under Section 397(3)(b) for TDS deducted from:

- Salary income under Section 392, or

- Income of a specified senior citizen under Section 393(1), for the relevant quarters ending June, September, December, or March.

6. Change in Quarterly TDS Statement for Non-Salary Payments

The quarterly TDS statement for all non-salary payments, presently submitted as Form No. 26Q, shall be renamed Form No. 140. It is submitted under Section 397(3)(b) for reporting tax deducted on non-salary payments incurred during the pertinent quarter.

7. Change in Quarterly TDS Return for Non-Resident Payments

The current Form No. 27Q, which is the quarterly TDS return for payments made to non-residents (other than salary), will be renumbered as Form No. 144. This is particularly relevant for businesses that engage foreign consultants, make royalty payments abroad, or process international contractor payments.

8. Form No. 168 to Replace Form No. 26AS – Annual Information Statement

The Annual Information Statement (AIS), which is currently presented in Form No. 26AS, is set to be renumbered as Form No. 168 according to the Draft Income-tax Rules, 2026. Form 26AS is one of the most frequently referenced documents by employees and Finance teams during ITR filing, as it consolidates all TDS deductions, advance tax payments, and financial transaction data linked to a PAN.

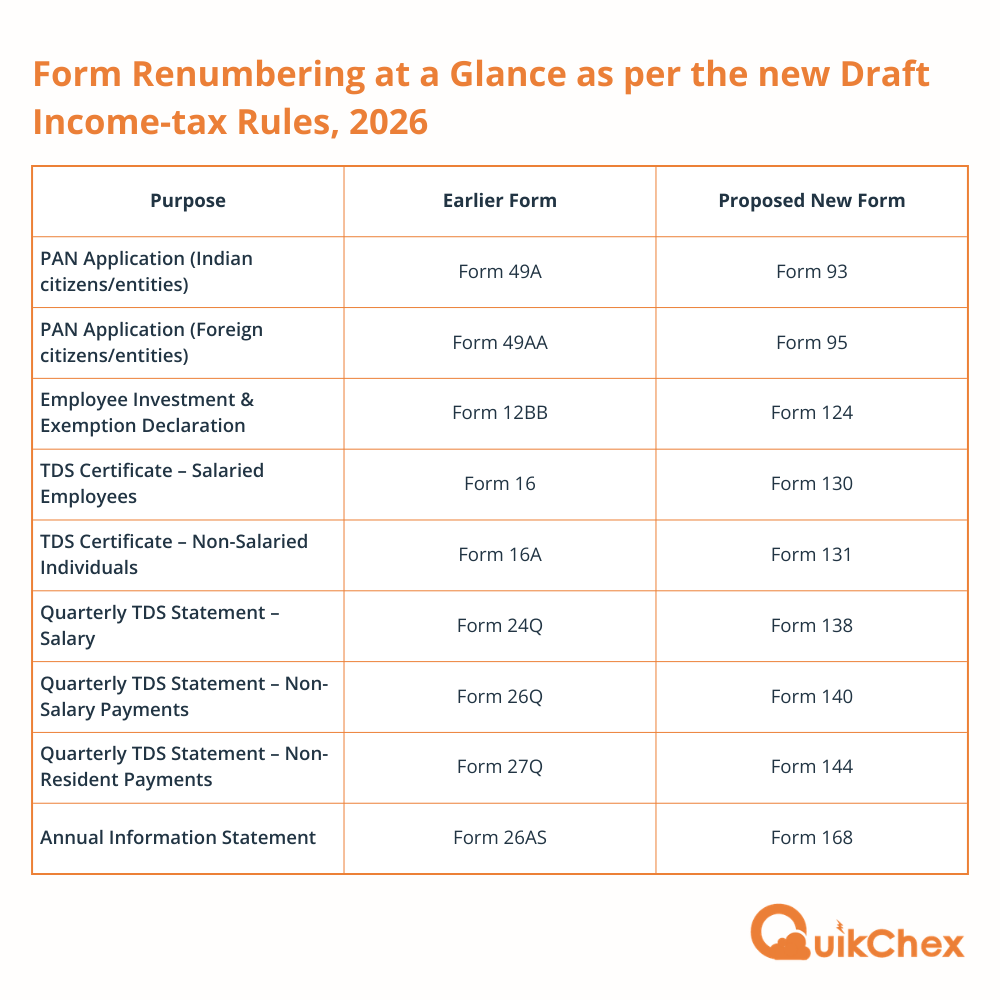

Quick Reference: Form Renumbering at a Glance

Purpose | Earlier Form | Proposed New Form |

PAN Application (Indian citizens/entities) | Form 49A | Form 93 |

PAN Application (Foreign citizens/entities) | Form 49AA | Form 95 |

Employee Investment & Exemption Declaration | Form 12BB | Form 124 |

TDS Certificate – Salaried Employees | Form 16 | Form 130 |

TDS Certificate – Non-Salaried Individuals | Form 16A | Form 131 |

Quarterly TDS Statement – Salary | Form 24Q | Form 138 |

Quarterly TDS Statement – Non-Salary Payments | Form 26Q | Form 140 |

Quarterly TDS Statement – Non-Resident Payments | Form 27Q | Form 144 |

Annual Information Statement | Form 26AS | Form 168 |

Click here to download the quick reference guide for form renumbering under the new Draft Income-tax Rules 2026.

{kind=link}

Important: Any payroll software, HRMS platform, or manual process that continues to generate the old form numbers post April 1, 2026 will be filing non-compliant returns. Ensure your payroll partner has updated their system to generate all statutory outputs under the new form numbers before your April payroll cycle begins, or you can migrate to Quikchex.

Gray Areas, Anticipated Situations, & How to Mitigate Them

While the Draft Income-tax Rules, 2026 aim to simplify compliance, the transition introduces several anomalies and new administrative burdens. Here are the most prominent conflicting scenarios HR and Finance teams will face in April 2026, and how to proactively mitigate them.

Situation A: The HRA “Landlord Relationship” Conflict

The government is cracking down on fake House Rent Allowance (HRA) claims by demanding stricter disclosures.

The Problem

Salaried taxpayers claiming HRA with annual rent exceeding ₹1,00,000 are now required to explicitly disclose their “relationship with the landlord” in the newly proposed Form 124. While paying rent to parents or a spouse is not expressly illegal, this mandatory disclosure flag will trigger automated scrutiny by the Income Tax Department’s systems.

The Risk for Employers

If an employee submits rent receipts from a relative, employers are caught in the middle. Approving the exemption without thorough checks could lead to compliance disputes during audits.

How to Mitigate

HR teams must issue a clear, updated HRA policy immediately. Employers should adopt a digital ESS portal that mandates employees to submit secondary proofs (e.g. bank transfer statements and the landlord’s ITR showing the rent as taxable income) before the HRA claim can be processed by payroll.

Situation B: Employee Tax Shock Due to Company Cars

Because the taxable value of employer-provided cars has drastically increased to reflect modern inflation, executives will see a sudden spike in their TDS.

The Problem

An employee using a small company car (≤1.6L) with a driver previously had a perquisite value of just ₹2,700/month. Under the new rules, this jumps to ₹8,000/month.

How to Mitigate

This update will shrink monthly take-home payouts. HR teams must proactively communicate this change to affected employees before April 2026. Employers should consider restructuring compensation packages—such as shifting employees to the expanded HRA metro limits or utilizing the newly increased meal, education, and hostel allowances—to neutralize the tax impact.

Situation C: Leaving Money on the Table for Meals & Education

The Problem

If your current payroll policy is strictly tied to the old 1962 limits, your employees will lose out on massive new tax-saving potential under the Old Tax Regime.

How to Mitigate

To act in the interest of employees, finance teams must redesign their flexi-benefit structures. Employees should be allowed to opt-in for meal vouchers up to ₹200 per meal (up from ₹50). Furthermore, HR should educate employees about the monumental jump in the Children Education Allowance (from ₹100 to ₹3,000/month per child) and the Hostel Allowance (from ₹300 to ₹9,000/month per child).

Situation D: Data Localization vs. Cloud HRMS

A significant compliance anomaly arises not in the calculations, but in HR and Finance data storage.

The Problem

The revised Tax Audit forms embedded in the Draft Rules now mandate that companies explicitly disclose details of:

- Their accounting software

- Cloud storage locations

- IP addresses, and crucially,

- Physical backup servers located in India.

The Risk for Employers

Many Indian businesses opt for global HRMS software with no managed services, that host data on servers in the US or Europe. Under the strict new reporting norms, utilizing a payroll system without compliance to the new draft rules, could complicate tax audit clearances.

How to Mitigate

Businesses must urgently audit their software vendors and ask them to comply ASAP. Moving to a domestic, 100% India-made and India-hosted HRMS like Quikchex ensures absolute compliance with these new data localization and audit disclosure mandates.

How Are Quikchex Customers Prepared for the new Draft Income-tax Rules 2026?

For Quikchex clients, whose payroll is managed through a dedicated SPOC (Single Point of Contact), the transition to the new financial year will be supported directly by the assigned payroll team. Your assigned Quikchex SPOC will review and rework the employee CTC structures considering:

- Proposed Income-tax Rule changes under Draft Income-tax Rules, 2026

- Applicable Labour Code related changes

- Revised perquisite valuation rules

- Updated allowance exemption limits

Based on these changes, the payroll team will prepare revised salary structures (CTC break-ups) wherever required.

This approach ensures that payroll structures remain compliant, optimised, and aligned with the latest regulatory changes, while giving clients full visibility and approval before any modifications are applied.

As the government moves toward a “Smart Form,” digital-first ecosystem, Quikchex guarantees that your payroll remains 100% compliant, accurate, and completely stress-free.

The Conclusion for the new Draft Income-tax Rules 2026

The Draft Income-tax Rules, 2026 signal the end of “easy forms for complex facts.” Tax administration is becoming entirely digital for centralized processing and automated reconciliation. To ensure your business transitions seamlessly without compliance penalties or frustrated employees, upgrading to an automated payroll and compliance ecosystem is no longer an option—it is an operational necessity.

Based on the new rule changes, payroll structure changes must be initiated effective 1st April 2026, running parallel with the pending New Wage Code changes, which is, again, pending for final draft.

Important Note: These Tax rule changes will be applicable only for employees opting for the Old Tax Regime.

Disclaimer: These are Draft Rules, and final notifications are awaited. Quikchex will continue to monitor developments and share further updates once the rules are notified by the CBDT.